Assessing profit shifting using country-by-country reports: a non-linear response to tax rate differentials

Research by Bratta, Santomartino & Acciari 2021

Summary

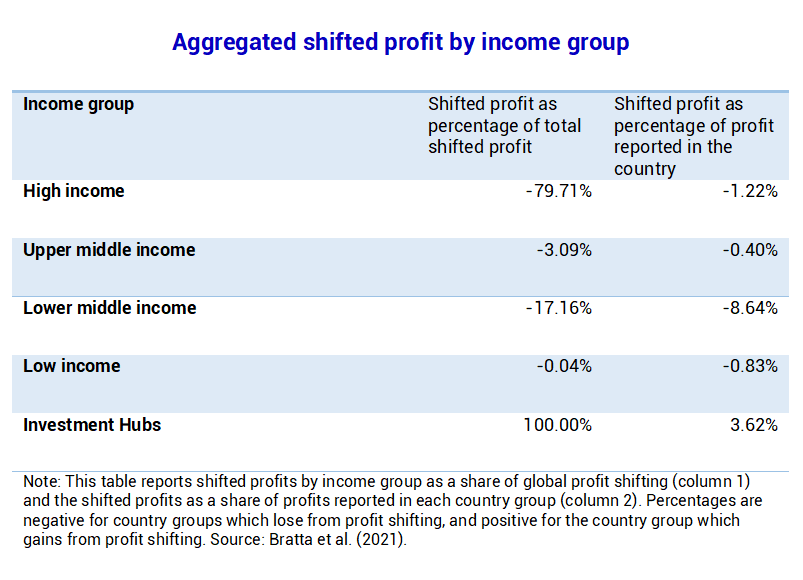

Bratta, Santomartino, and Acciari estimate the scale of global profit shifting and the associated corporate income tax (CIT) revenue losses. Their estimation is based on confidential Country-by-Country Reports (CbCRs) for 2017, by all multinational enterprises (MNEs) headquartered in Italy or having at least one subsidiary in Italy. They use statutory and effective tax rates to test whether the allocation of profits by MNEs depends on the level of CIT rates in each country or on the differences of CIT rates in between countries. If MNEs report significantly more profits in low-tax countries than in high-tax countries and if this cannot be explained by economic activity or other control variables, it might indicate that they shift profits to low-tax countries to reduce their global tax payments. The authors find that the effect of the CIT rate differential on the location of profit is particularly significant. Consistently with previous studies, they also find strong evidence of a non-linear relationship, which implies that most of MNEs’ profit shifting seems to be directed towards countries with very low tax rates while tax rate differentials between countries with average and high tax rates seem to play a minor role for profit shifting. Extrapolating from their sample to the total global population of MNEs, the authors estimate that, in 2017, a total of € 887 billion of profits was shifted due to differences in tax rates which resulted in a global revenue loss of € 245 billion – a finding broadly in line with previous results. A per-country disaggregation suggests that investment hubs are the main destination of shifted profits, and high-income countries lose most in absolute terms while lower middle-income countries lose most in relative terms.

Key results

- In 2017, a total of € 887 billion of profits was shifted due to differences in tax rates with a global revenue loss of € 245 billion.

- Global profit shifting is highly concentrated in a few countries: 80% of total shifted profits involves seven countries of origin and eight jurisdictions of destination.

- Investment hubs are the main destination of shifted profits and high-income countries are the ones losing more profits due to profit shifting.

- the statutory corporate income tax rate in a given country

- the tax rate differential, meaning the difference between the statutory CIT rate of the country where the subsidiary is located and the average CIT rate faced by the other subsidiaries of the same group located in all other countries

- the tax rate differential using forward-looking effective average tax rates.